MoFo Report

The Impact of the Covid-19 Outbreak on Asia Private Equity

03 Apr 2020

The Impact of the Covid-19 Outbreak on Asia Private Equity

Following our recent webinar “After the Outbreak: How Will the COVID-19 Outbreak Impact the Future of PE Transactions in Asia?” we surveyed legal and investment professionals from private equity funds that are based in or that have significant investments in Asia.

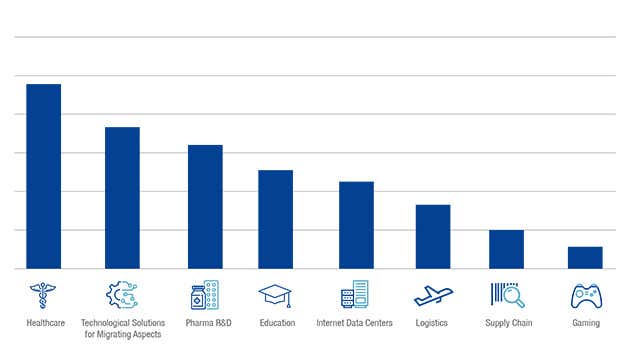

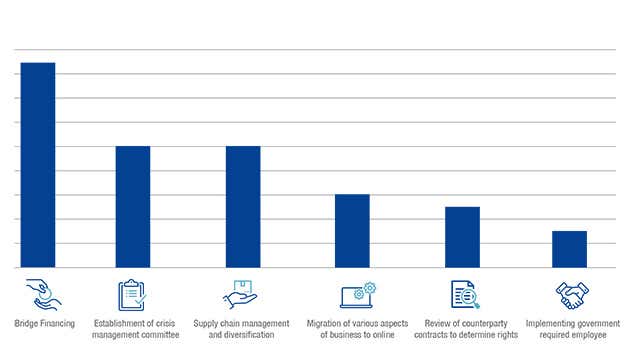

We have summarized the results of the study into five key findings to provide a snapshot of the current and long‑term impact of the COVID-19 outbreak on PE investments, the management of portfolio companies and the business operations of private equity funds.*

MoFo Insights

MoFo Insights

MoFo Insights

MoFo Insights

MoFo Insights

*67% of the funds surveyed are headquartered in Asia, with over US$1 billion in AUM respectively. 23% of the respondents come from funds with over US$20 billion under management.